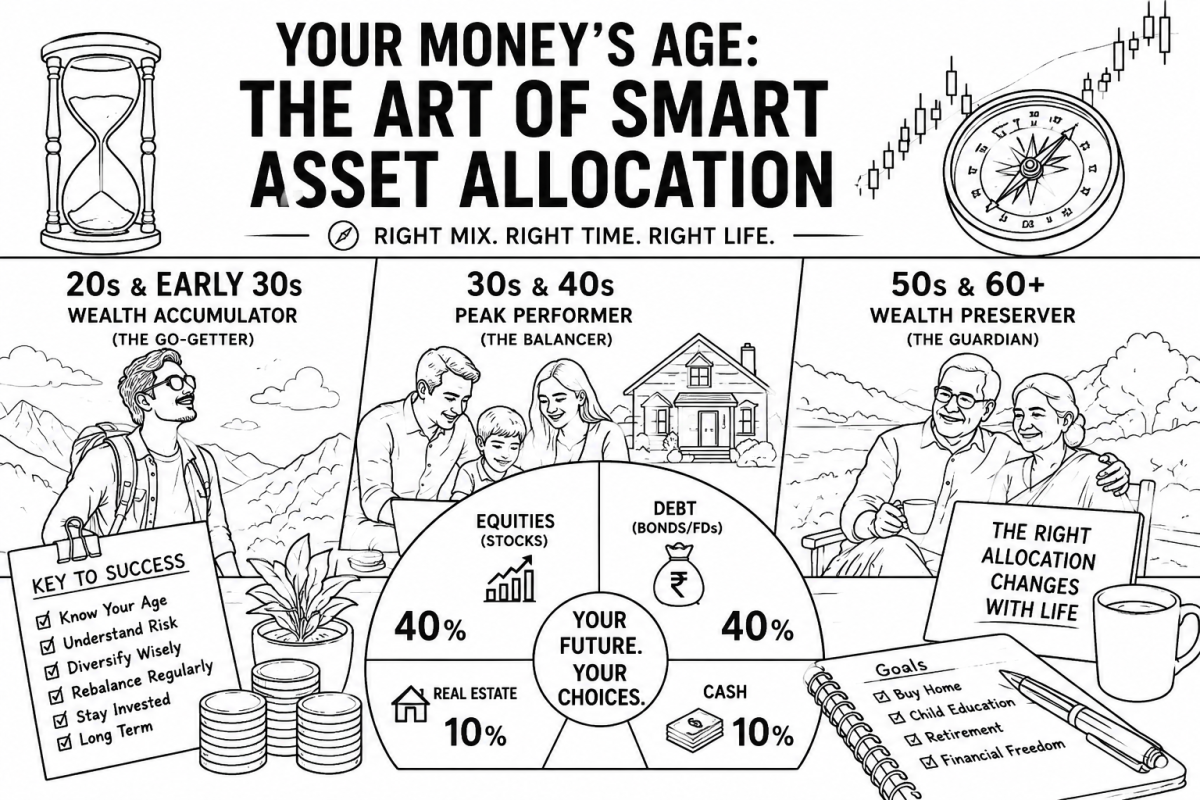

Think of your investment portfolio like your body. At 25, you can handle spicy street food and adventurous treks. At 55, you might prefer a balanced diet and a brisk walk. Similarly, your money needs a diet plan that changes with your life’s age. This is the essence of Asset Allocation – the single most important decision in your financial journey.

It’s not about picking the “hottest” stock; it’s about strategically dividing your money between asset classes: Equities (Stocks), Debt (Bonds/FDs), Real Estate, and Cash. And this mix must evolve as you do.

The Rationale: It’s Psychology, Not Just Finance

Why change the mix? It boils down to two things: Time and Sleep.

- Time is your greatest ally. It allows you to ride out the wild swings of the stock market. A 25-year-old has decades for their investments to recover from a market crash. A 55-year-old does not.

- Sleep is your daily performance metric. Can you sleep peacefully if your portfolio value drops 30% in a market correction? If not, your allocation is too aggressive for your psychological risk profile.

Let’s break down the age-based blueprint, inspired by proven strategies.

The Blueprint for Your Financial Life

The 20s & Early 30s: The Wealth Accumulator (The “Go-Getter”)

- Mantra: Aggressive Growth.

- Sample Allocation: 80% Equities, 15% Debt, 5% Cash.

- Rationale: You have the ultimate advantage – time. Your earning years are ahead. You can afford to take risks. This is the time to be heavily invested in equities (stocks, equity mutual funds) through SIPs. A market fall is a fire sale, not a disaster. Think of it as buying your favourite brand at a discount. In India, this is the time to tap into the long-term growth story of sectors like technology, renewables, and consumption.

The 30s & 40s: The Peak Performer (The “Balancer”)

- Mantra: Growth with Stability.

- Sample Allocation: 60% Equities, 30% Debt, 10% Real Estate/Gold.

- Rationale: You’re likely in your prime earning years, but also juggling EMIs, children’s education, and ageing parents. Your portfolio needs a shock absorber. You continue chasing growth with equities but start building a solid foundation with debt (PPF, Debt Mutual Funds, NCDs). This balances risk and ensures you don’t derail your goals during a market downturn.

The 50s & 60+: The Wealth Preserver (The “Guardian”)

- Mantra: Capital Preservation & Income.

- Sample Allocation: 40% Equities, Debut 50% Debt, 10% Cash.

- Rationale: Retirement is near or here. Your focus shifts from earning more to not losing what you have. Your portfolio should generate a steady income. Debt instruments (Senior Citizen Savings Scheme, POMIS, Annuities) become the cornerstone. However, keeping a portion in equities is crucial to fight inflation and ensure your money doesn’t run out. A 5% inflation will halve your purchasing power in 14 years!

The Indian Twist: It’s Personal!

This blueprint is a guide, not a gospel. Your allocation must be personal.

- Are you a single entrepreneur at 40? You might afford a more equity-heavy portfolio than a salaried peer with two kids in international school.

- Do you have a government pension? Your reliance on your portfolio for income is lower, allowing for more risk.

- Does market volatility give you anxiety? Scale back equities, even if you’re young. Peace of mind is an asset no one can price.

Final Thought: Your asset allocation is the compass for your financial ship. The destination changes—from buying a car to funding a wedding to a peaceful retirement. Regularly recalibrate this compass (a process called rebalancing) as you sail through different seasons of life. Start today, because in finance, as in life, the right move at the right time makes all the difference.

Disclaimer: This is for academic purposes. Please consult your financial advisor before making any investment decisions.